Deal valuations and deal multiples tend to decline as market uncertainty manifests itself, most simply, in higher discount rates on longer term cash flows within valuation models. This is part of the cyclical deal pricing process that occurs during credit tightening (“crunches”) e.g., 2008 and since 2022.

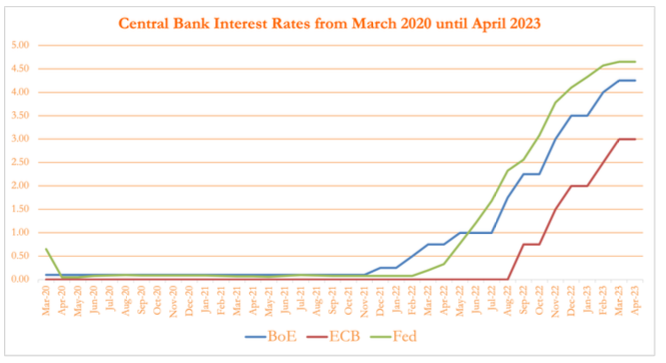

In stark contrast to the capital superabundance of the past few years influenced by historically expansive monetary polices across the global economy, since the second half of 2022 deals worldwide have experienced a significant drop-off. As Warren Buffett said recently during a trip to Japan, “interest rates are to asset prices what gravity is to the apple” due to their impact on the WACC (weighted average cost of capital) from a valuation perspective, but more generally on the cost of borrowing money either to finance investment given the relative cost vs. equity sales and the tax benefit in most jurisdictions. Observing three main Central Bank rates since the fallout of COVID reflects the intensity of this gravitation that has been felt across asset classes:

Figure A

Source: William John Analytics, Bank of England, Federal Reserve & European Central Bank

Despite rising interest rates, tougher financing and falling valuations, it can present an opportunity for deal practitioners.

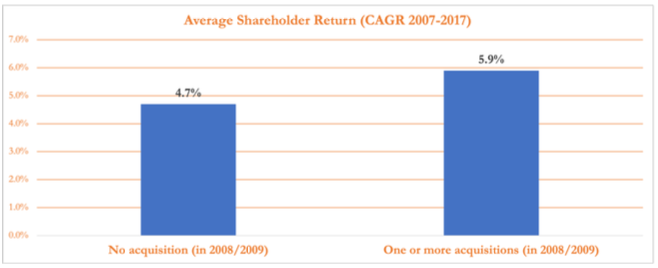

In Bain’s Global M&A Report 2023, they analysed the acquisition activity of 2,485 companies from around the world during the Financial Crisis in 2008 and 2009. They found that companies that made one or more acquisitions during 2008 or 2009 had a 120-basis point higher average shareholder return based on the compound average growth rate (CAGR) between 2007 – 2017:

Figure B

Source: William John Analytics, Dealogic, Bain Consulting

Moreover, in 2007, worldwide deals surpassed 40,000 for the first time and the cumulative deal value hit $4.6 trillion, 40% above the dotcom peak in 2000. In other words, despite cyclical swings in deal activity and valuations, over the long run deal value and activity continues to hit new heights and it is in those cyclical lulls that opportunity exists for savvy dealmakers.

What is that opportunity? For strategic M&A, the last recession saw some of the most industry defining deals for the past two decades or so, including the following three cases:

- 1) StanleyWorksacquisitionofBlack&Decker:Black&Decker,avictimofitsdemand exposure to the construction lull after the financial crisis, witnessed a 22% drop in revenue and 41% drop in earnings before interest and taxes which substantially lowered the company’s valuation.

- 2) Pfizer’sacquisitionofWyethfor$68.4billion:Inearly2009,thisagreementbought Pfizer time as many of the patents of its leading medicines were about to expire. Furthermore, it gave the company time to diversify its pharmaceuticals portfolio and expand its pipeline.

- 3) DisneyacquisitionofMarvel:Inthesecondhalfof2009,DisneyacquiredMarvelfor $4.2 billion with several strategic motives, including the well-known success of the “Marvel Cinematic Universe”.

What stands out about these deals in particular is that all three acquirers had two things in common. One, they have an experienced and repeatable M&A strategy. For example, Stanley Works has a proven post-merger integration capability built from an aggressive M&A programme since 2002, acquiring 33 companies over the next several years. Two, all three acquisitions were already aligned to the company mission and overarching strategy, either by strengthening the core business, increasing scale (and economies of), or creating strategic options.

Generalising this, average total shareholder returns for the Bain research can be broken down further into the following matrix:

Figure C

Source: William John Analytics, Dealogic, Bain Consulting

What this data shows is that companies who are “active acquirers” outperform bystanders during economic downturns. But it is not just frequency of deals that contributes to greater total shareholder returns, it is also “materiality” – how much M&A is transacted as a proportion of market capitalisation 3 months prior to deal announcement, also known as cumulative relative deal value, see below:

Figure D

Source: William John Analytics, Dealogic, Bain Consulting

The matrix above validates the idea that frequent acquirers can use their experience and skillset developed over time deal to deal to execute deals more effectively and generate higher total shareholder returns than those who do not. It also shows that the largest deals undertaken by frequent acquirers generate the highest returns.

Based on this research, despite the high gravitational effect of current interest rates and the overall macroeconomic environment, opportunities do exist for companies who have deep M&A experience to add value to their business and execute strategic deals – in fact the data shows that during the last more severe Financial Crisis, such a strategy added the most value for shareholders. Hence, M&A activity in 2023 may continue to underperform relative to the highs in 2021 and perpetuate a cyclical downturn. But, on past experience, opportunities exist to transact some of the most significant deals for the next decade.

Any opinions expressed in this document are those of William John and are provided for information only. E&OE