The semi-sensationalist macroeconomic turmoil observed in the UK since the Brexit vote in June 2016 puts the country in a league of its own, despite a once in a century pandemic almost decimating capitalism as we know it across the globe without some creative Keynesian intervention.

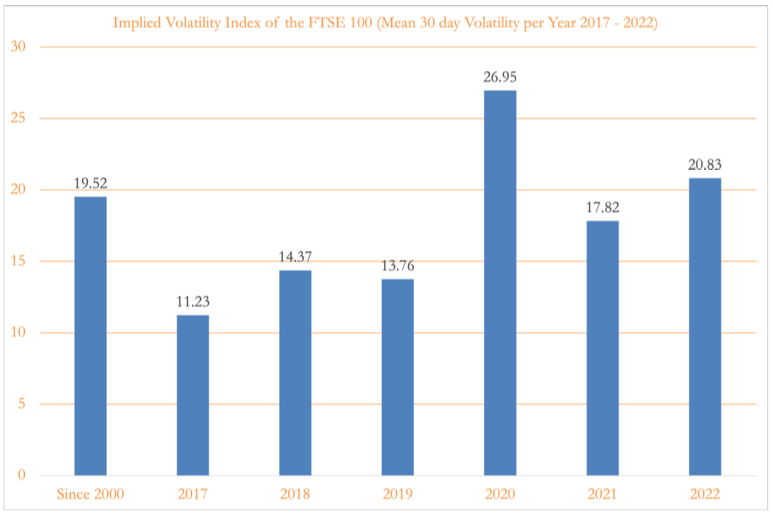

Looking at the Implied Volatility Index of the FTSE 100 since 2017 compared to the average since 2000:

Figure A

Source: William John Analytics, FTSE Russell

Implied Volatility (IV) captures the market view of the likelihood of changes in future security prices. In this case the share prices of the top 100 companies listed in U.K. markets by market capitalisation. When it rises it often indicates greater market uncertainty about the future state of the market – and by extrapolation the economy. In fact, according to the FTSE Russell factsheet on this index (FTSE 100 IVI), the FTSE 100 and the FTSE 100 IVI have had a -0.59 correlation since 2000, based on 30-day implied volatility. In simper terms, when one tends to move up, the other significantly but moderately moves in the opposite direction.

Taking this metric alone, when average implied volatility is trending upwards since 2019 and above average since 2000, this would indicate U.K. markets are bearish about the future of U.K. companies, and by extension the U.K. economy.

However, this metric looks at future stock price movements alone, and of that the future expected price movements of large cap UK companies. Hence, it is important to dig deeper into other economic fundamentals to determine the base case for the economy moving forwards.

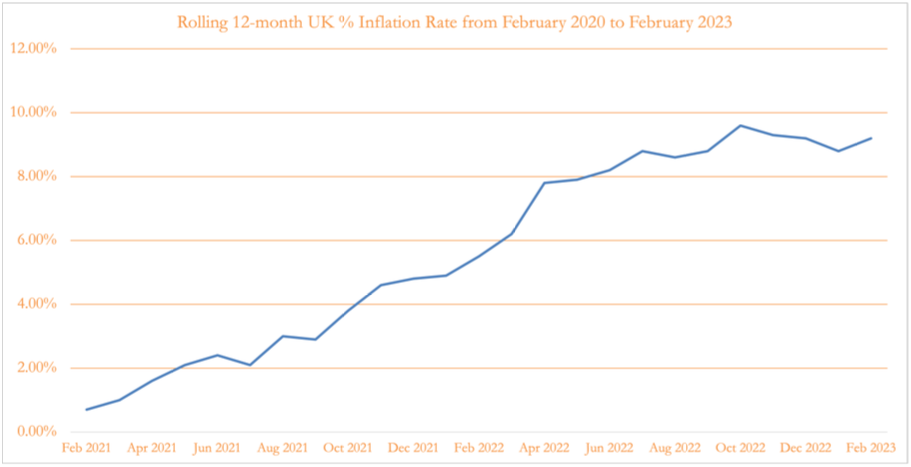

Looking at the % GDP growth and UK inflation rate over the past few years paints a pretty bleak picture:

Figure B

Source: William John Analytics, Office for National Statistics

Figure C

Source: William John Analytics, Office for National Statistics

UK GDP has been stagnating for the past year or so, whilst the UK inflation rate has been rapidly climbing for the past two years, approaching an 8% premium on the traditional Bank of England benchmark of 2% inflation per year (on a rolling basis). This “stagflation” (stagnant economic growth combined with high inflation) will have an adverse effect on the economy as it implies, in aggregate, that prices of goods and services are increasing at a rate faster than the total spending in the UK.

This inflation has been largely exacerbated by high energy prices resultant of the Ukraine war, as depicted below:

Figure D

Source: William John Analytics, Office for National Statistics

Note: Y axis unit = %

Direct energy, and very high, high, and low energy intensive goods & services make up the vast majority of the rise in the inflation rate since Q1 2021.

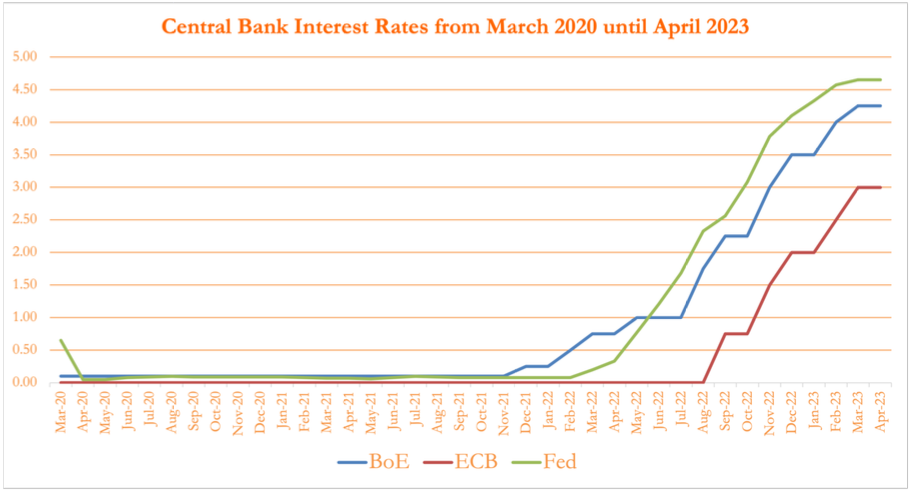

Figure E

Source: William John Analytics, Bank of England, Federal Reserve & European Central Bank

The issue with this policy is that it is likely to cause “sticky” inflation in the current environment. Sticky inflation results from “cost-push” inflation and low economic growth (aka stagflation) due to the fact Central Banks are constrained to aggressively raising interest rates in order to protect aggregate demand, and, higher inflation expectations, i.e., when people expect higher inflation it is more difficult to reduce it. A practical demonstration of this is the recent unionisation of major public services bargaining for higher wages because of the pressure on the cost of living resulting from higher inflation.

In a stagflationary environment made up of “sticky” inflation that is unlikely to substantially reduce in an immediate forecast, it is likely GDP will fall in the next year at least. Whether this meets the definition of a technical recession of three consecutive quarters of negative GDP growth or not remains to be seen and there is nothing to suggest it would be a deep recession with mass unemployment, low investment etc. However, it could be sustained for longer relative to 2008 as Central Banks balance reducing the inflation rate with its impact on investment and the cost of living for households.

Hence, in these circumstances, the base case for the UK economy in the next 5 years ought to be a mild recession.

Any opinions expressed in this document are those of William John and are provided for information only. E&OE