Private credit, or the provision of debt financing by funds, companies or investors rather than banks, bank-led syndicates or public markets, has emerged as a significant force in recent years. Many institutions, such as Fidelity International and Apollo Capital Management, are making significant provisions to include this segment in their portfolio strategies and asset allocations over the coming decade, according to a recent article written by Bloomberg.

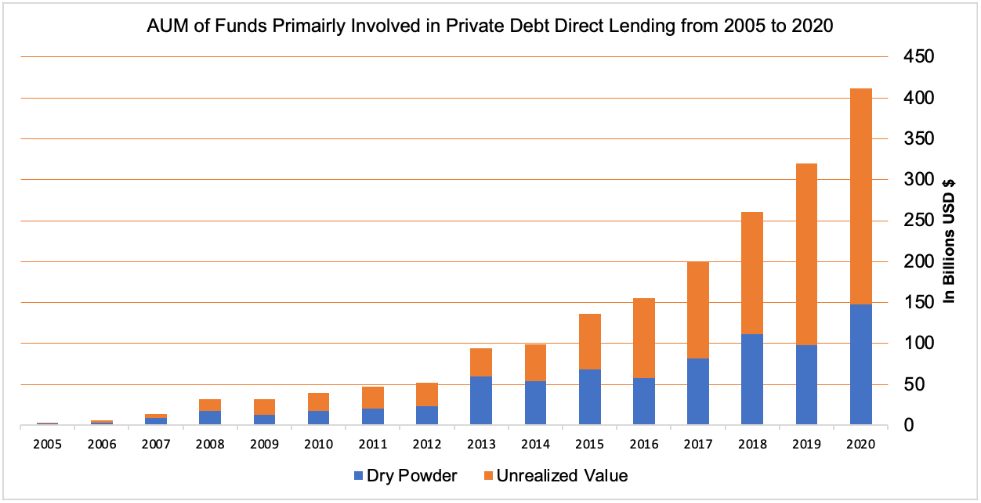

In fact, the private debt market has grown ten-fold in the past decade or so, with assets under management of funds (primarily) involved in direct lending surging to an unprecedented $412 billion by the end of 2020:

Figure A

Source: William John Analytics, S&P Global

There are numerous factors which may be driving the growth in this asset class. Firstly, there has been a prolonged low interest rate environment, which may have compelled investors to seek higher yielding assets, and subsequently alternative investment strategies such as private credit.

Secondly, tightening regulatory frameworks imposed on traditional lending in the aftermath of the financial crisis, such as the Dodd-Frank Wall Street Reform and Consumer Protection Act, has left gaps in the market where private creditors can capture value. For instance, the increasing need for capital in underserved markets such as small and medium sized enterprises, who aren’t worth the regulatory risk to large banking syndicates but may offer tremendous value to investors willing to do their due diligence.

Thirdly, the rise of FinTech platforms has facilitated the growth of private credit. These platforms provide efficient access to borrowers and lenders, streamlining loan origination and are enhancing transparency. Technology-driven underwriting and data analytics have also improved risk assessment capabilities, enabling private credit providers to make informed lending decisions.

These macroeconomic factors may have accelerated the investment in the asset class, however the competitive advantages of the asset class over syndicated debt are independently desirable for underserved markets and investors seeking appealing yields.

Private credit differs from Syndicated Debt in a variety of ways. Private credit involves direct lending between a borrower and private lenders, offering tailored terms and structures based on specific needs. It relies on established relationships, emphasizing trust and personal connections as well as complex contractual covenants, such as equity warrants or options under certain conditions, for example.

Moreover, they are non-public, providing privacy and flexibility with less regulatory oversight. Given these factors, these deals can be complex, requiring in-depth due diligence, but very rewarding if done correctly.

In contrast, syndicated debt is publicly traded and listed on exchanges, attracting a diverse investor base. It follows standardized terms, allowing for price discovery and transferability. Publicly issued debt is subject to regulatory oversight, with companies adhering to disclosure requirements, ensuring transparency and reassurance to investors.

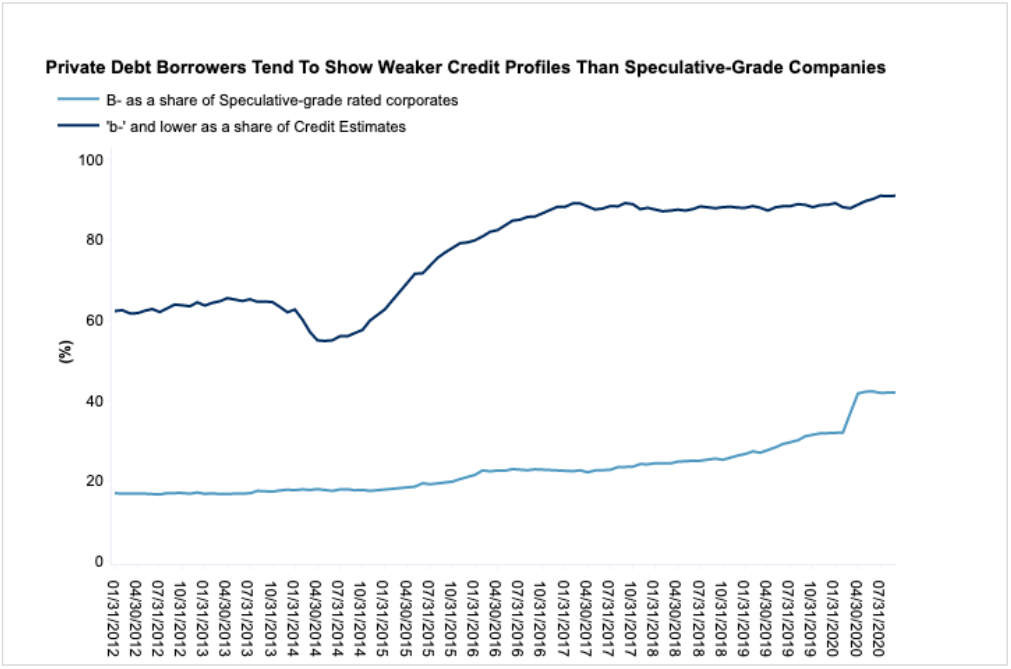

Whilst private credit has gained popularity and witnessed significant growth, it is not without some valid risks and pitfalls. Chief among these is the lack of transparency and regulatory oversight in private credit markets. This opacity makes it challenging for investors to fully assess the risks and credit quality of their investments.

For example, looking at credit estimates of private debt borrowers vs. speculative grade

companies between 2012 and 2020:

Figure B

Source: William John Analytics, S&P Global

Private credit borrowers tend to have approximately 40% more weaker credit profiles that speculative grade debt in public markets.

Moreover, the absence of consistent valuation practices in private credit markets poses challenges for investors and regulators alike. The illiquid nature of private credit assets, combined with the absence of standardized methodologies for valuing these assets, makes it difficult to accurately assess their fair value. This ambiguity can lead to potential mispricing and discrepancies in reported performance.

The final concern revolves around investor protection. Private credit investments often involve complex deal structures, varying levels of leverage, and diverse risk management strategies. The lack of standardized practices and regulatory oversight raises questions about investor safeguards and the potential for systemic risks.

The most notable (and infamous) example of this would be the collapse of Lex Greensill’s Supply Chain Finance Income (SCF) fund in 2021. The fund relied heavily on securitizing invoices into investment products and faced challenges related to the creditworthiness of some of its borrowers. The collapse highlighted the potential dangers of overexposure to certain industries and clients, as Greensill’s significant reliance on the GFG Alliance conglomerate led to concerns about concentration risk.

Furthermore, Greensill’s complex funding arrangements and lack of transparency regarding its operations raised red flags. The intricate web of relationships between Greensill, its clients, and its investors made it difficult for stakeholders to fully grasp the extent of the company’s financial obligations and risks. These issues underscore the risks of private credit, including the potential for inadequate risk assessment, insufficient due diligence, and the concentration of exposure to specific borrowers or industries.

In conclusion, the boom in private credit has been driven by a combination of macroeconomic factors and competitive advantages over syndicated debt. The prolonged low interest rate environment, tightening regulatory frameworks, and the rise of FinTech platforms have all contributed to the growth of private credit as an alternative investment strategy.

However, while private credit offers appealing yields and tailored terms, it also carries inherent risks. The lack of transparency and regulatory oversight in private credit markets poses challenges for investors in assessing credit quality and accurately valuing assets. These risks highlight the need for robust risk management practices, thorough due diligence, and effective regulatory oversight in the private credit industry. Standardized valuation methodologies, increased transparency, and investor safeguards are essential to mitigate the pitfalls and protect the interests of all stakeholders involved.

As private credit continues to grow and attract investors, it is crucial to strike a balance between reaping the benefits of this asset class and managing the associated risks. The lessons learned from high-profile failures and the ongoing efforts to enhance industry practices will shape the future of private credit, ultimately determining its long-term sustainability and its role in the broader financial landscape.

Any opinions expressed in this document are those of William John and are provided for information only. E&OE