In recent years, the global oil market has exhibited remarkable volatility, driven by a confluence of factors. Geopolitical tensions, supply-demand dynamics, and economic uncertainties have contributed to significant price fluctuations.

Meanwhile, the emergence of the COVID-19 pandemic in 2020 introduced unprecedented disruption, precipitating a substantial decline in oil demand amid widespread travel restrictions and economic lockdowns, and even leading to negative prices for contracts of barrels of Oil. Concurrently, the escalating global emphasis on renewable energy and heightened environmental concerns has accelerated the industry’s shift towards sustainable alternatives, thereby reshaping the long-term trajectory of the oil market.

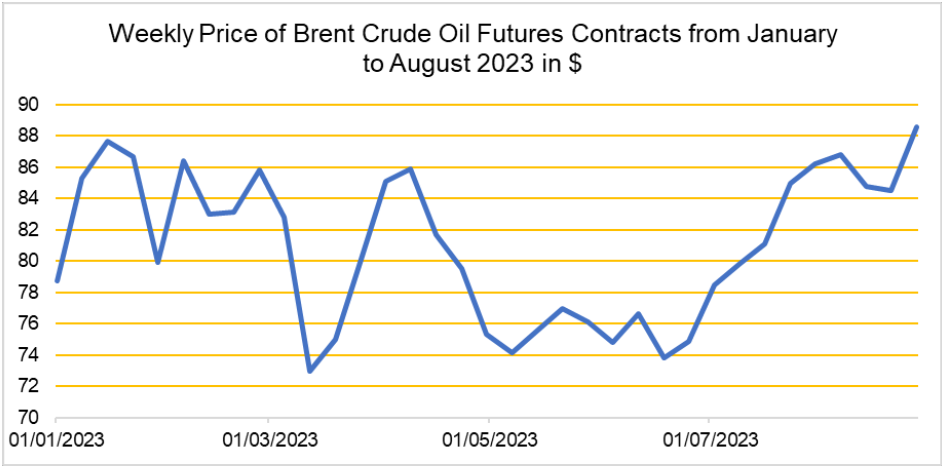

However, over the summer of 2023, global Oil demand has surged dramatically to a record peak of 103 million barrels a day in June, according to revised estimates by the International Energy Agency, and for the year, global oil demand is on track to expand 2.2mb/d to 102.2 mb/d – its highest ever annual level. This surge in demand has been reflected in the price for Brent crude oil, for example:

Figure A

Brent crude oil futures have gained 12.44% YTD.

These record highs have been attributed to strong summer air travel, increased oil use in power generation and surging Chinese petrochemical activity. In fact, China accounts for more than 70% of global oil demand expansion in 2023 to date, with many analysts attributing this to demand for Naphtha (a versatile feedstock in petrochemical production, a solvent in various industries, and a component in gasoline blending) and Kerosene, two key industrial petrochemicals.

Breaking down the growth int OPEC+ and Non-OPEC+ oil producers, a sharp reduction in Saudi production in July saw output from the OPEC+ bloc fall 1.2 mb/d to 50.7 mb/d, while non- OPEC+ volumes rose 310 kb/d to 50.2 mb/d. Global oil output is projected to expand by 1.5 mb/d to a record 101.5 mb/d in 2023, with the US driving non-OPEC+ gains of 1.9 mb/d. Next year, non-OPEC+ supply is also set to dominate world supply growth, up 1.3 mb/d while OPEC+ could add just 160 kb/d.

The impact of this record demand is that refineries find themselves in a quandary as they grapple with meeting burgeoning demand, contending with challenges like the shift to new feedstocks, operational disruptions, and heightened temperatures, necessitating many operators to scale back production.

Despite robust gasoline and diesel markets, propelling profit margins to a six-month zenith, naphtha faces sustained pressure owing to the dual impact of competitive liquefied petroleum gas (LPG) prices and sluggish petrochemical activity beyond China. Notably, there’s been a considerable tightening in high-sulfur fuel oil as refiners substitute lost OPEC+ crude with lighter grades, marking a historical milestone with high-sulfur fuel oil in Rotterdam surpassing North Sea Dated for the first time in 28 years.

This confluence of factors has led to a marked reduction in crude and product inventories, with observed oil stocks seeing a third consecutive monthly decline in July. OECD industry stocks now stand more than 100 million barrels below the five-year average. Projected tightening market balances in the fall stem from the extended supply cuts by Saudi Arabia and Russia, slated to endure at least through September. Despite a considerable OPEC+ spare capacity cushion of 5.7 million barrels per day, allowing room for the alliance to ramp up output later in the year, adhering to current production targets could deplete oil inventories by 2.2 million barrels per day in 3Q23 and 1.2 million barrels per day in the fourth quarter, potentially exerting upward pressure on prices.

Looking ahead, extended supply cuts by major players may further tighten market balances, posing a potential risk of depleting oil inventories and exerting upward pressure on prices, emphasizing the intricate and resilient nature of the global oil market

Any opinions expressed in this document are those of William John and are provided for

information only. E&OE