In recent fiscal quarters, the performance of American equities has been a testament to the robust nature of its financial markets. Amidst a backdrop of global economic challenges, U.S. stocks have exhibited remarkable resilience and dynamic growth, showcasing the agility of the American financial system. Technological innovation, strategic fiscal policies, and the intrinsic resilience of corporate entities have collectively propelled the equity market on an upward trajectory.

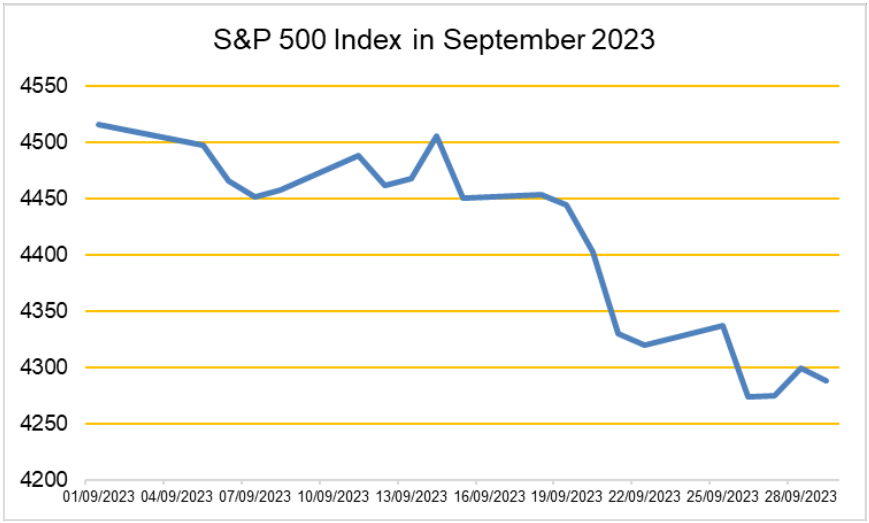

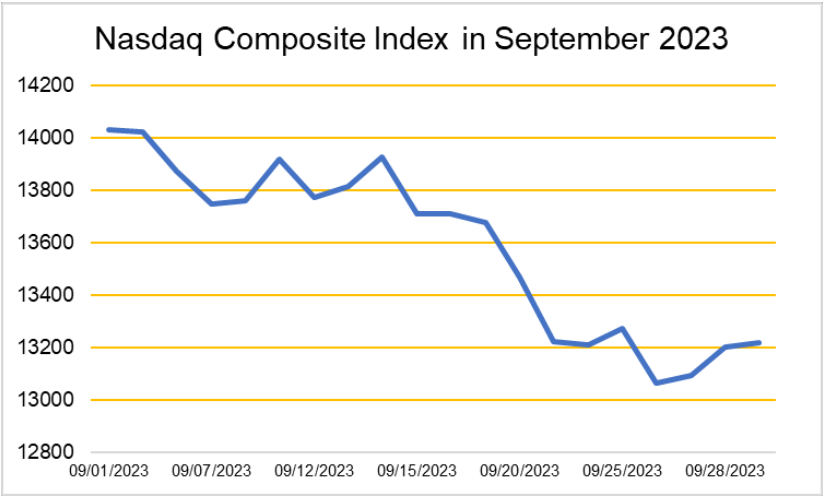

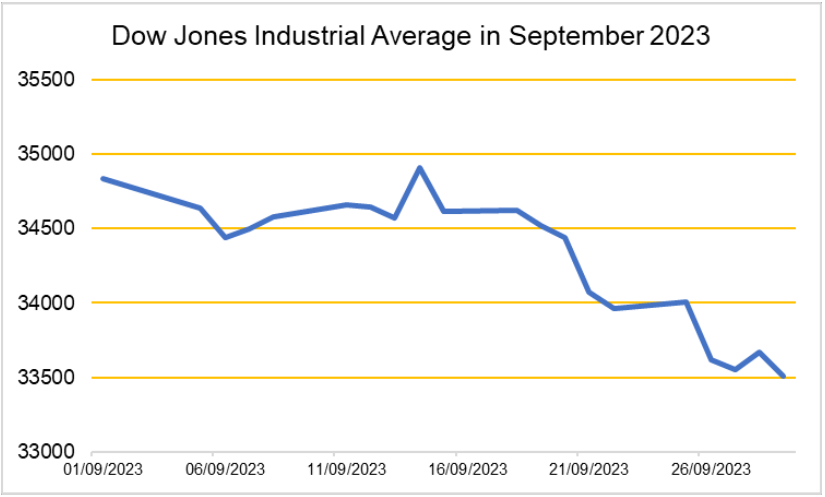

However, in the month of September, all three major equity indices, namely the S&P 500; Dow Jones Industrial Average and the Nasdaq Composite all ended in red, with negative returns of 4.87%, 3.5% and 5.81% respectively to make it the worst performing month for stocks since December 2022:

Figure A

Source: William John Analytics, S&P Global

Figure B

Source: William John Analytics, Nasdaq

Figure C

Source: William John Analytics, Yahoo Finance

A common excuse concerning equity performance in September is known as “the September Effect”. This is a phenomenon that refers to the historical tendency for stock markets to underperform during the month of September. While the exact reasons for this pattern are debated, several theories offer insights.

One theory attributes the September Effect to investors returning from summer vacations and reassessing their portfolios, leading to increased selling pressure. Additionally, mutual funds often close their books in September, prompting portfolio adjustments. Behavioural finance theories suggest that psychological biases, such as fear and caution, may influence investor decisions during this period because of these theories.

Furthermore, historical events, such as market crashes in September (e.g., 1929 and 2008), contribute to a perception of September as a risky month, potentially influencing investor behaviour and exacerbating market volatility.

Assessing the month of September practically, stock markets faced headwinds primarily driven by a complex interplay of factors, resulting in a notable decline across the stock markets. The pivotal influence was the resurgence of Treasury yields, reaching 4.58%, their highest level since 2007. This spike in yields reflected the market’s acceptance of an enduring high-interest- rate environment, as the Federal Reserve aimed to curb persistent inflation.

The inverse relationship between Treasury yields and stock prices became evident, with investors less inclined to pay elevated prices for stocks and opting for the perceived safety of Treasuries.

Economic concerns compounded the market’s unease. While recent data indicated a slight cool-down in inflation and tempered consumer spending growth, these factors, while potentially alleviating inflationary pressures, also hinted at a potential slowdown in economic momentum. The resumption of student loan repayments, coupled with rising oil prices and the looming threat of a federal government shutdown, further added to the economic challenges faced by investors.

Conclusively, the formidable performance of American equities in recent fiscal quarters, characterized by resilience and growth, faced an unprecedented setback in September 2023.

This downturn is commonly attributed to the “September Effect,” historically marked by underperformance, but the pivotal driver was the resurgence of Treasury yields to 4.58% and compounding economic concerns, including tempered inflation, cooling consumer spending growth, rising oil prices and the looming threat of a government shutdown further intensified market unease.

Any opinions expressed in this document are those of William John and are provided for

information only. E&OE