Nothing in the global economy has deeper reverberations than that of central banking interest rates, that orchestrate the delicate balance between economic stability and growth. Beyond the numerical metrics, these rates wield substantial influence over a spectrum of financial variables, impacting borrowing costs, investment strategies, and overall economic vitality.

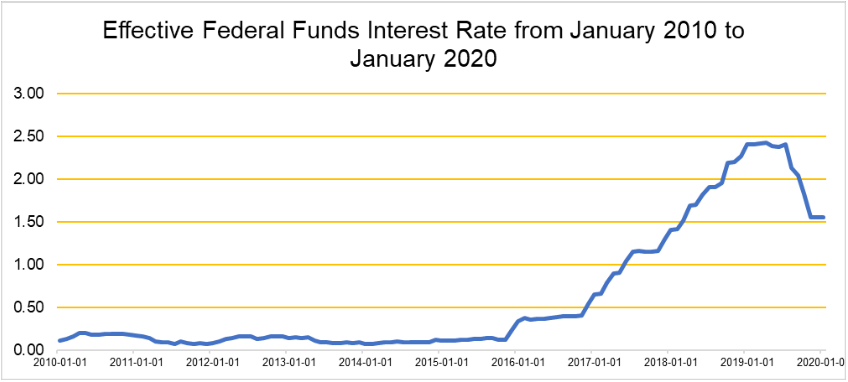

Throughout the 2010s, Western central banks, exemplified by the U.S. Federal Reserve and the European Central Bank (ECB), initially responded to the 2008 financial crisis with historically low interest rates and quantitative easing. In the mid-2010s, signs of economic improvement led to attempts at normalization, with the U.S. initiating interest rate hikes. However, by the late 2010s, global uncertainties prompted a shift to a more accommodative stance, as seen in the Federal Reserve’s rate cuts in 2019 to sustain economic growth. Assessing the U.S. Federal Funds rate throughout the 2010’s:

Figure A

Source: William John Analytics, Federal Reserve

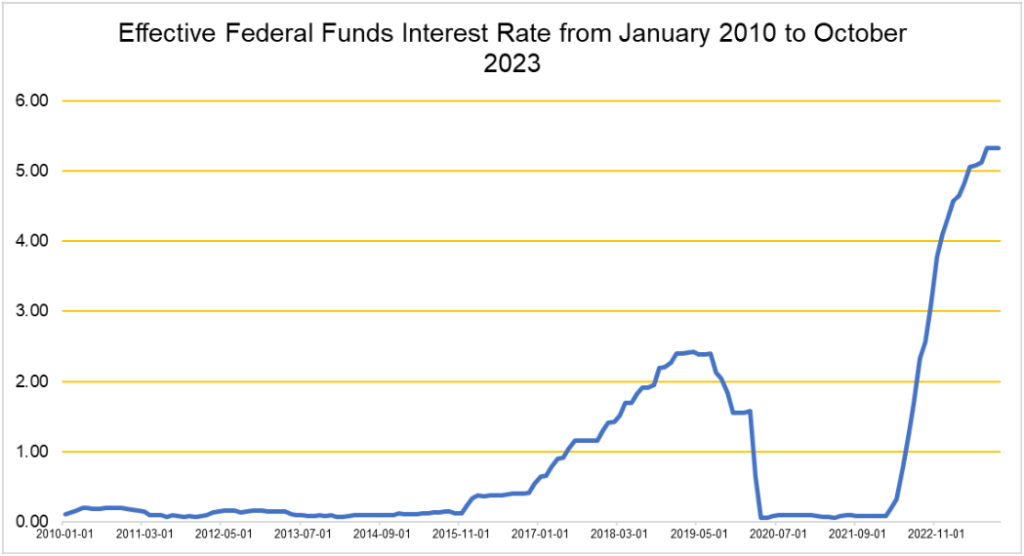

With the fallout of the COVID-19 pandemic in 2020, this prompted both Western and Eastern central banks to implement aggressive monetary measures, including rate cuts and stimulus programs, to counteract the economic fallout:

Figure B

Source: William John Analytics, Federal Reserve

However, the geopolitical impact of Russia’s invasion of Ukraine on energy prices combined with the economic supply shocks and bottlenecks generated by pandemic lockdowns then caused an aggressive hike in interest rates to levels not seen since the 1980s:

Figure C

Source: William John Analytics, Federal Reserve

The consequences of these interest rates in recent times has impacted almost every market in all their different forms: capital, property and money.

As central banks implement rate hikes, the cost of borrowing for individuals and businesses rises, leading to reduced consumer spending and diminished business investments. Meanwhile, the housing market is experiencing a slowdown due to increased mortgage rates, while the stock market is exhibiting heightened volatility. Those with variable-rate debt face challenges in servicing their obligations and so investors have been watching central banks closely as inflation slows:

Figure D

Source: William John Analytics, U.S. Bureau of Labor Statistics

Taking the U.S. economy as an example, inflation has slowed from a high of 9.1% Y/Y in June 2022 to 3.2% as of October 2023 – just 1.2% off the status quo nominal target of 2% Y/Y.

The significance of subdued inflation lies in its ability to preserve the purchasing power of a currency, offering consumers the assurance that their money will retain its value over time. This climate of low inflation fosters a predictable environment for businesses and consumers alike, enabling more effective long-term planning and investment decisions.

As inflation remains in check, central banks are inclined to keep interest rates relatively low. This translates into a boom for borrowers, as the cost of obtaining capital becomes more affordable. The resulting encouragement for businesses to invest and expand can contribute to economic growth and job creation.

Furthermore, a low inflation rate reduces uncertainty in financial markets. Investors find a more stable footing for decision-making, as the eroding effects of rapidly rising prices are mitigated. This, in turn, promotes a healthier and more resilient financial landscape.

Thus far, this slowdown in the rate of inflation is leading to speculation that Central Banks may begin cutting their rates, and these more predictable expectations for consumers, businesses, investors, and governments will only boost economic prosperity and investment in the long run.

Any opinions expressed in this document are those of William John and are provided for information only. E&OE