Inflation not experienced across the West since the oil crisis of the 1970s, war raging in Eastern Europe reminiscent of the Cold War and interest rates soaring to combat inflation all points to dark skies ahead for national Aggregate Demand and national product, and international financial prosperity.

Comparing macroeconomic data from the ’70s with now lends credence to the comparisons in the media and pundits alike.

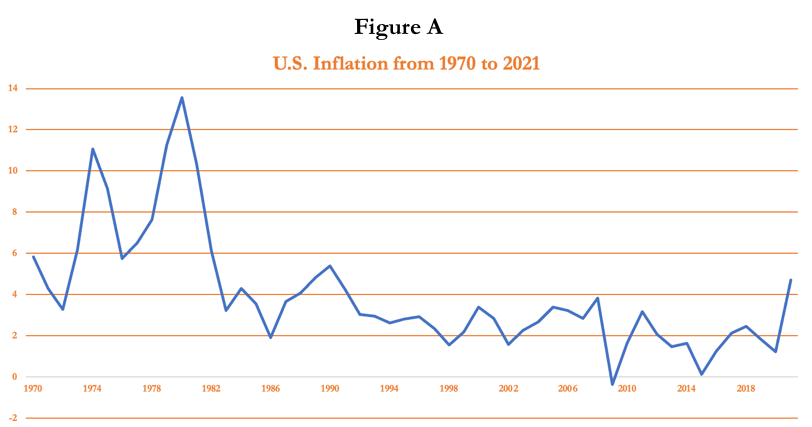

Due to the World Bank and International Monetary Fund (IMF) not tracking World composite inflation data until 1981, U.S inflation was selected instead to demonstrate the effects of inflation that was felt by major economies during the Oil Shocks, including the U.K, Spain, France and Australia.

Source: World Bank, William John Analytics

The spot price of Brent Crude Oil represents the options market value for crude oil produced in the North Sea.

Common practice is to find the average Spot Price for Dubai, Western Texas Intermediate, and Brent crude oils to reflect the price of oil globally, however Brent nevertheless remains a good reflection due to its history and availability of data.

In fact, it has been found that 40% of all American dollars printed ever, were printed in 2021 (at least theoretically). Read more here.

Source: Trading Economics, William John Analytics

In both cases, the 1970s and today, there are many similarities. Inflation has been fuelled by a supply side shock resulting from surging energy costs (both derived from oil and other hydrocarbons like natural gas). Interest rates are on the rise, having been hiked 6 times (U.S. example) from 0.25% to 4.75% as of Feb 23’, evoking similar memories to the aggressive hiking of interest rates during the ’70s and both circumstances come from a highly, Keynesian monetary stance of printing money at historic highs and lowering borrowing costs to historic lows (in the latter case to push economies through a global pandemic).

These macroeconomic factors, combined with weak GDP growth:

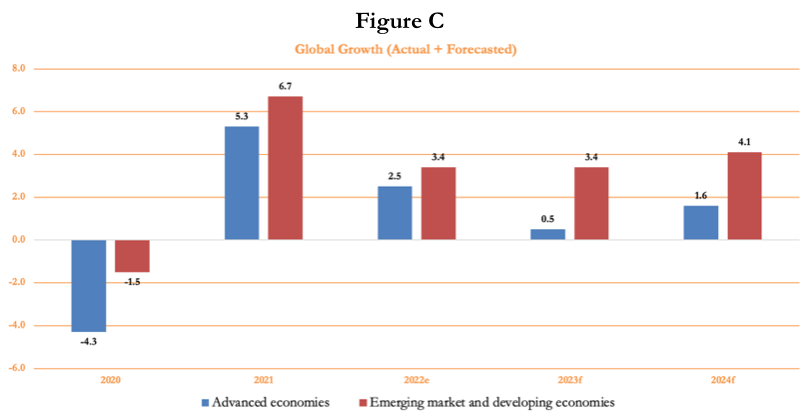

“Advanced economies” included: the U.S., Eurozone, and Japan whilst “Emerging market and developing economies” included countries from Sub-Saharan Africa, parts of Europe, Latin America, and the Middle East.

Source: World Bank, William John Analytics

According to the report by the World Bank, “Global growth is projected to slow to its third-weakest pace in nearly three decades, overshadowed only by the 2009 and 2020 global recessions”.

However, it should be noted that all these metrics have hit neither the gradient nor the magnitude of the shocks experienced in the ’70s, where for example oil prices quadrupled in 1973-74 and doubled in 1979-80. So, whilst the two situations are comparable, they are not congruent.

Nevertheless, based on these approximations, in the 1970s, there were two global recessions and a financial crisis following sustained high inflation, soaring interest rates & energy costs, and lagging global economic growth, aka a “stagflationary” environment. Thus, putting two and two together, one can make a reasonable base case for a recession at least in Western economies in the immediate future.

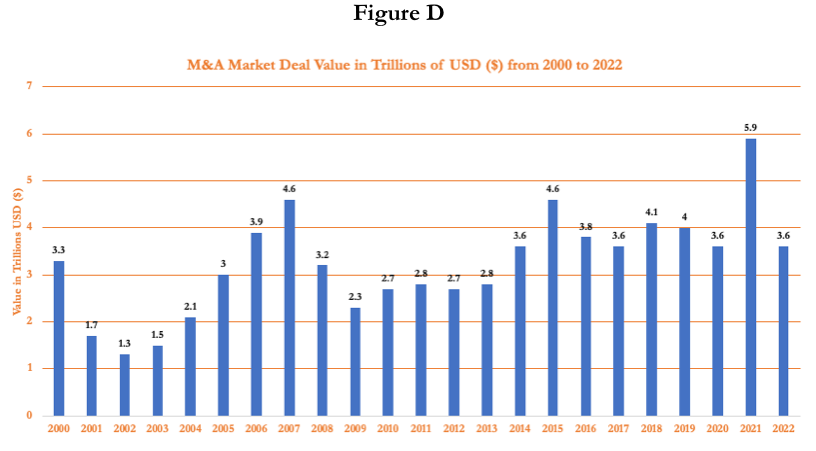

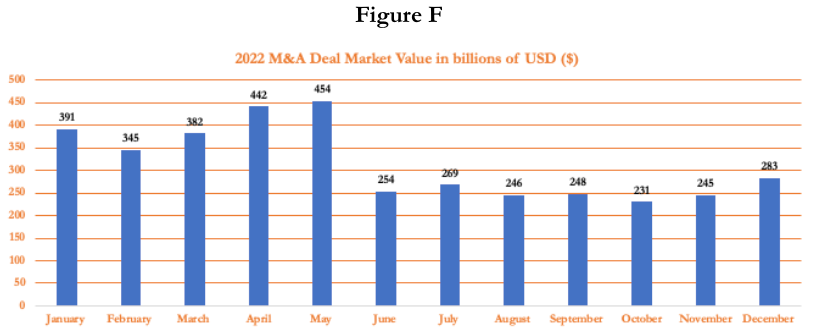

So what did this mean for M&A in 2022?

Coming off record high deal activity in 2020 and 2021, the compound annual growth rate for all M&A (2021-2022) was -36%. Looking at the value of M&A deals from 2000 to 2022:

Stagflation, a term coined by British politician Iain Macleod, refers to a poor combination of stagnant economic growth coupled with high inflation.

For more information on comparing the 1970s economic backdrop to today, see this article.

Source: Bain Consulting, Dealogic, William John Analytics

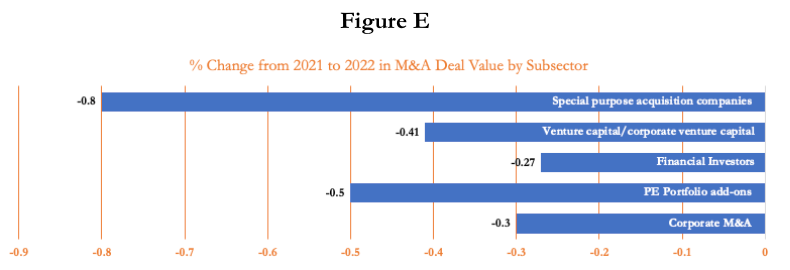

Clearly, as the macroeconomic environment has transformed from a loose and accommodating monetary policy environment to a stagflationary one, the M&A market has had a substantial reversal in fortune.

Analysing the year-on-year change in M&A deal value by subtype:

Source: Bain Consulting, Dealogic, William John Analytics

Special Purposes Acquisition Companies, or “SPACs” saw a major decline, but all major types of M&A saw a substantial decline. Focusing on 2022 specifically – the year was “a tale of two halves.”

Source: Bain Consulting, Dealogic, William John Analytics

There is no doubt that the market has felt the effects of a steep increase in “economic uncertainty”, leading to this reduction in deal volume and hence deal value.

Structural Uncertainty

Inflation, interest rates, capital liquidity and availability, national security and geopolitical tensions are just a few factors that are currently deeply embedded in investor decision making concerning capital allocation.

In an era of capital superabundance, following a reversal in monetary policy across economies, investors are clearly more intrigued by rising costs of capital (aka borrowing for leverage). It should be noted that the leveraged buyout is not the only means of acquisition, referring here to stock and cash which is another conversation, however those stakeholders who rely on debt (private equity investors etc.) are definitely feeling the effects of these new founded “capital constraints”.

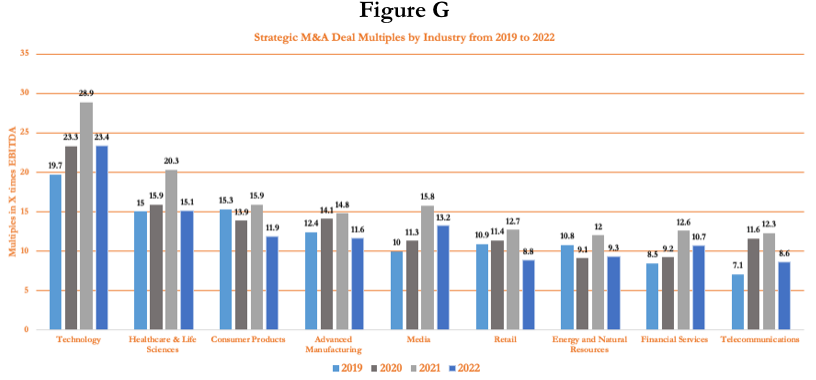

Capital constraints and economic uncertainty have contributed to a drop-off in deal multiples. Looking at industry median enterprise value to EBITDA multiples on strategic deals from 2019 to 2022:

Source: Bain Consulting, Dealogic, William John Analytics

Discount rates are derived from the cost of capital, and risks associated with economic uncertainty amongst other factors.

Deal multiples may have decline as higher discount rates on cash flow valuation have resulted in an investor premium on nearer term cash flows over longer-term growth. It’s worth noting that this decline was mirrored in the public capital markets. For example, the S&P 500 has declined significantly from its approximate 4,800-point highs in 2021.

Looking ahead to 2023

Overall, a stagflationary and gloomy macroeconomic picture has contributed to a shift in M&A strategic valuation and M&A deal value & volume has shrunk considerably from the record highs in 2020 and 2021. Looking ahead to 2023, it will be interesting to see how these trends evolve.

Any opinions expressed in this document are those of William John and are provided for information only. E&OE.