In January 2023, Prime Minister of the United Kingdom Rishi Sunak set out three economic priorities: to halve inflation, grow the economy and reduce debt.

These three key imperatives require transparent and careful fiscal and monetary management. As such, the Government and Bank of England must navigate the delicate task of curbing inflationary pressures without hampering economic activity, steer efforts towards productivity and investments for a sustainable recovery, all while addressing the imperative to strategically reduce national debt.

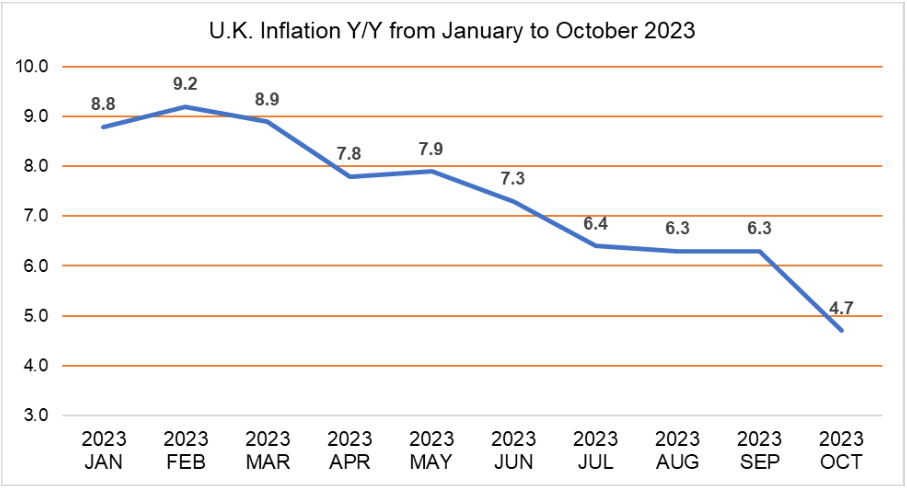

Looking at the progress of inflation since the pledge in January 2023:

Figure A

Source: William John Analytics, Office for National Statistics

Clearly, this month inflation has hit the Prime Minister’s target, and subsequently, should inflation continue to drop towards the nominally ideal target of circa 2%, this will have several positive impacts on the U.K economy and its citizens.

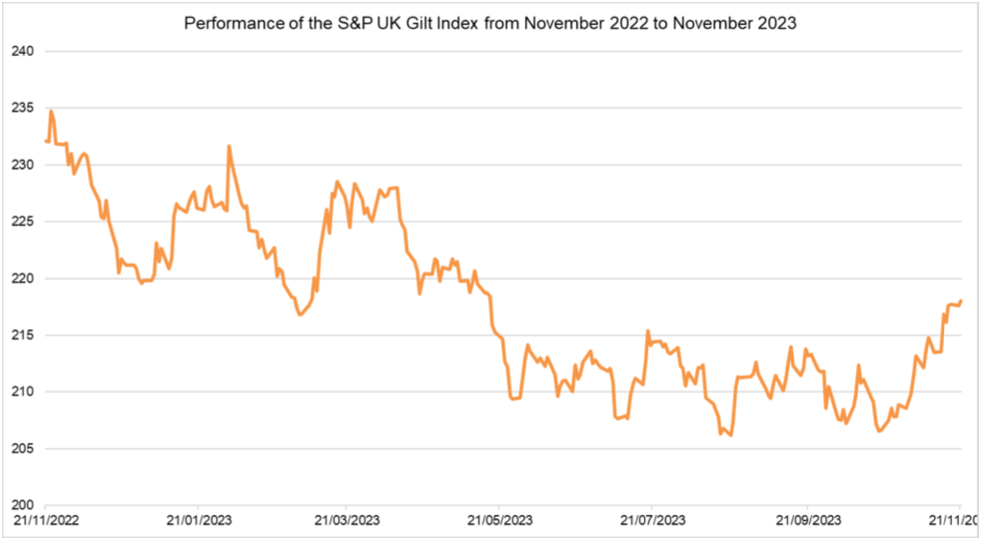

Falling inflation will stabilise people’s real incomes aka their “purchasing power” fostering consumer confidence and perhaps generate a reversal of slowing consumer spending in recent months. This “consumer confidence” may also be reflected in the fixed income public markets for similar reasons, preserving the value of people’s pensions, savings and interest on fixed income instruments. If this trend continues, it could boost the value of the U.K. Gilt Market, which offered investors a -6.06% return between November 2022 and November 2023:

Figure B

Source: William John Analytics, S&P Global

Additionally, falling inflation will grant certainty to commerce and business expectations in the foreseeable future, which will only aid the government with its other two pledges, stimulating growth and reducing debt.

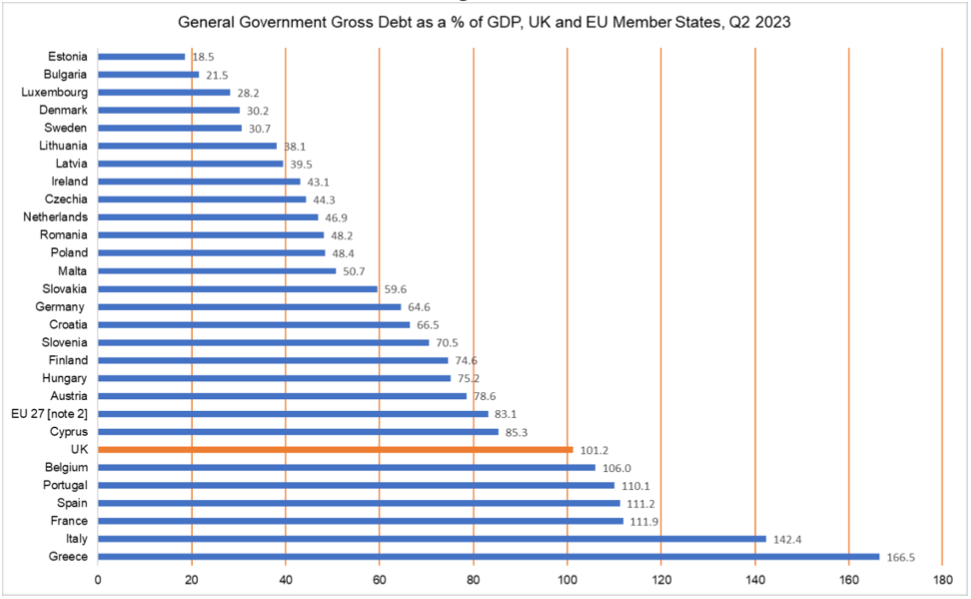

U.K. debt was £2,639.9 billion at the end of Q2 2023 (April to June), equivalent to 101.2% of Gross Domestic Product (GDP). Comparing this to the European average:

Figure C

Source: William John Analytics, Office for National Statistics

It is 18.1 percentage points above the EU average and hence a mixture of time and excellent fiscal policy will be required to bring it in line with the EU 27.

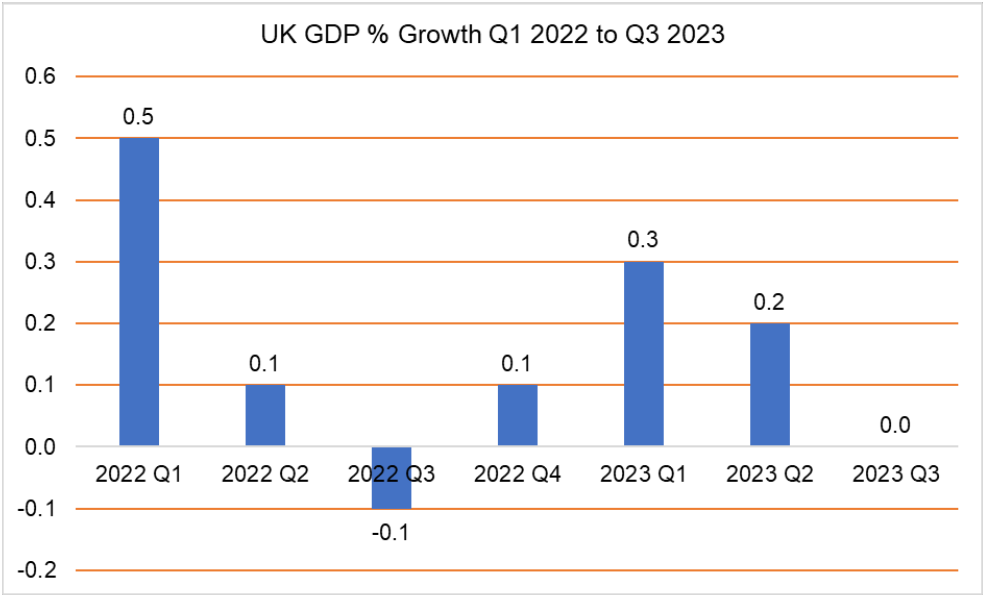

Meanwhile, the U.K. has experienced four consecutive quarters of non-negative growth since Q4 2022, putting it at least 6 months away from a technical recession. Assessing U.K. GDP growth since the start of 2022:

Figure D

Source: William John Analytics, Office for National Statistics

Therefore, in order to hit the Prime Minister’s aims of reducing national debt as a % of GDP whilst growing GDP (a common measure of economic growth), it is clear that the Government will pursue policies aimed at boosting Aggregate Demand (Consumer Spending, Public Spending, Investment or Net Exports) whilst keeping government borrowing constant or reductive.

These policies are likely to be outlined in the Chancellor’s Autumn Statement being released imminently. In the meantime, the current economic landscape in the U.K. reflects a harmonious triad of falling inflation, stable economic growth, and an ambitious target for national debt.

Any opinions expressed in this document are those of William John and are provided for information only. E&OE